What Robinson nails is the way that this is what Scaramucci does — it’s his job. Scaramucci is a fund-of-funds manager, posting returns even he admits are lackluster: he more or less tracks the S&P 500, while making big, risky bets (a third of his assets are in MBS), investing in leveraged hedge funds, and reserving the right not to redeem his clients’ money upon request. Which means that he only has two ways to make money: either find stupid people to give him their money, or else shower himself with so many conspicuous indicia of success that people just want to buy into his perceived success.

OK, make that one way to make money.

It’s far from clear that Scaramucci actually is successful, in financial terms, by Wall Street standards. He certainly spends a lot — millions of dollars — on various forms of conspicuous consumption and self-promotion. But he’s not making a lot: since he’s a fund-of-funds manager, he’s making 1.5-and-zero, rather than 2-and-20. And under the terms of his deal with Citigroup, a substantial chunk of that 1.5 goes straight to them. He has to run Skybridge, of course, with all the employee compensation, compliance costs, and the like that entails. He’s regularly writing seven-figure checks to pay for things like the Davos Tasting of ludicrously expensive wine. And of course he has to pony up charitable donations, too, so as to be able to get up in front of a well-heeled crowd to receive the Hedge Funds Care Award for Caring. (I’m not making this up.)

Scaramucci’s fake-it-till-you-make-it approach might end up working: his fund is still growing, and Robinson says that he “has become the Wall Street player he aspired to be when he first landed at Goldman some 22 years ago.” He’s living proof of what Windward Capital’s Robert Nichols is quoted saying at the end of the article: “Performance isn’t what beats a path to your door. It’s sales and marketing.”

But he’s not a stock-picker, or even, really, a hedge-fund manager: he just plays one on TV.

Saturday, September 10, 2011

Remind me not to piss off Felix Salmon

Type M Bias

And classical multiple comparisons procedures—which select at an even higher threshold—make the type M problem worse still (even if these corrections solve other problems). This is one of the troubles with using multiple comparisons to attempt to adjust for spurious correlations in neuroscience. Whatever happens to exceed the threshold is almost certainly an overestimate.

I had never heard of Type M bias before I started following Andrew Gelman's blog. But now I think about it a lot when I do epidemiological studies. I have begun to think we need to have a two stage model: one study to establish an association followed by a replication study to estimate the effect size. I do know that novel associations I find often end up diluted after replication (not that I have that large of an N to work with).

The bigger question is whether the replication study should be bundled with the original effect estimate or if it makes more sense for a different group to look at the question in a separate paper. I like the latter more as it crowd-sources science. But it would be better if the original paper was not often in a far more prestigious journal than the replication study, as the replication study is the one that you would prefer to have the the default source for effect size estimation (and thus should be the easier and higher prestige one to find).

Friday, September 9, 2011

Replication in Science

The unspoken rule is that at least 50% of the studies published even in top tier academic journals – Science, Nature, Cell, PNAS, etc… – can’t be repeated with the same conclusions by an industrial lab. In particular, key animal models often don’t reproduce. This 50% failure rate isn’t a data free assertion: it’s backed up by dozens of experienced R&D professionals who’ve participated in the (re)testing of academic findings.

Of course, I worry even more about softer disciplines where the difficulties of replication are much higher (you don;t just have to replicate a lab, you may need to develop an entire new cohort study).

Scary stuff.

Thursday, September 8, 2011

Earmarks and Agricultural Research

Like so many bad trends in journalism, the archetypal example comes from Maureen Dowd, this time in a McCain puff piece from 2009. Here's the complete list of offending earmarks singled out by the senator and dutifully repeated by Dowd:

Before the Senate resoundingly defeated a McCain amendment on Tuesday that would have shorn 9,000 earmarks worth $7.7 billion from the $410 billion spending bill, the Arizona senator twittered lists of offensive bipartisan pork, including:Putting aside the relatively minuscule amounts of money involved here, the thing that jumps out about this list is that out of 9,000 earmarks, how few real losers McCain's staff was able to come up with. I wouldn't give the Autry top priority for federal money, but they've done some good work and I assume the same holds for the Polynesian Voyaging Society. Along the same lines, I have trouble getting that upset public monies spent on astronomical research. After that, McCain's selections become truly bizarre. Urban water usage is a huge issue, nowhere more important than in Western cities like Los Vegas and it's difficult to imagine anyone objecting to a program that actually gets kids out of gangs.

• $2.1 million for the Center for Grape Genetics in New York. “quick peel me a grape,” McCain twittered.

• $1.7 million for a honey bee factory in Weslaco, Tex.

• $1.7 million for pig odor research in Iowa.

• $1 million for Mormon cricket control in Utah. “Is that the species of cricket or a game played by the brits?” McCain tweeted.

• $819,000 for catfish genetics research in Alabama.

• $650,000 for beaver management in North Carolina and Mississippi.

• $951,500 for Sustainable Las Vegas. (McCain, a devotee of Vegas and gambling, must really be against earmarks if he doesn’t want to “sustain” Vegas.)

• $2 million “for the promotion of astronomy” in Hawaii, as McCain twittered, “because nothing says new jobs for average Americans like investing in astronomy.”

• $167,000 for the Autry National Center for the American West in Los Angeles. “Hopefully for a Back in the Saddle Again exhibit,” McCain tweeted sarcastically.

• $238,000 for the Polynesian Voyaging Society in Hawaii. “During these tough economic times with Americans out of work,” McCain twittered.

• $200,000 for a tattoo removal violence outreach program to help gang members or others shed visible signs of their past. “REALLY?” McCain twittered.

• $209,000 to improve blueberry production and efficiency in Georgia.

Of course, we have no way of knowing how effective these programs are, but questions of effectiveness are notably absent from McCain/Dowd's piece. Instead it functions solely on the level of mocking the stated purposes of the projects, which brings us to one of the most interesting and for me, damning, aspects of the list: the preponderance of agricultural research.

You could make a damned good case for agricultural research having had a bigger impact on the world and its economy over the past fifty years than research in any other field. That research continues to pay extraordinary dividends both in new production and in the control of pest and diseases. It also helps us address the substantial environmental issues that have come with industrial agriculture.

As I said before, this earmark coverage with an emphasis on agriculture is a recurring event. I remember Howard Kurtz getting all giggly over earmarks for research on dealing with waste from pig farms about ten years ago and I've lost count of the examples since then.

And interspaced between those stories at odd intervals were other reports, less flashy but far more substantial, describing some economic, environmental or public health crisis that reminded us of the need for just this kind of research. Sometimes the crisis is in one of the areas explicitly mocked (look up the impact of industrial pig farming on rural America* and see if you share Mr. Kurtz's sense of humor). Other times the specifics change, a different crop, a new pestilence, but still well within the type that writers like Dowd find so amusing.

Here's the most recent example:

Across North America, a tiny, invasive insect is threatening some eight billion trees. The emerald ash borer is deadly to ash trees. It first turned up in Detroit nine years ago, probably after arriving on a cargo ship from Asia. And since then, the ash borer has devastated forests in the upper Midwest and beyond.* Credit where credit is due. Though not as influential as Dowd, the New York Times also runs Nicholas Kristof who has done some excellent work describing the human cost of these crises.

Wednesday, September 7, 2011

"Ask Mister Math Person"

When a toothache is fatal

A commenter says that according to local news reports, he was quoted a price of $27 for the antibiotic (sounds like erythromycin, then), and $3 for a painkiller. I believe the former, but I have a very hard time swallowing the latter. I mean, I guess I could be wrong, but I am very skeptical that there is a pharmacy out there that sells more than a dose or two of any prescription painkiller for $3. If he chose to take two vicodin over antibiotics, when he must have known that this was not a long-term solution, I have to question his decision-making even more deeply.

But what this illustrates is just how hard it is to make a decision when in extreme levels of pain. I believe the legal term is "diminished capacity". Now, this sort of tragedy can happen under nationalized health care too. But imagine what happens if this type of decision making is extended to emergency rooms?

When good news is a long way away

These long-held concerns are now critical in a decade where the 79 million U.S. people born between 1946 and 1964 start retiring as soon as this year and larger boomer retirement waves build to peak around 2020-2022.

The concern is that the ebb and flow of U.S. stock markets over the past 50 years is highly correlated with the available pool of household savings channeled into equity investment.

Assuming peoples' prime savings years are those between ages 40 and 65, the proportion of the population in that bracket is therefore key to driving the market. As early as the 1980s, economists feared the impact this may have on U.S. housing markets -- and the recent real estate bust may owe it something -- but stock market connections are more convincing.

The data is alarming. Movements in the ratio of these high savers to both retirees and younger adults has presaged long cycles in real equity prices from the downward funk of 1970s to the subsequent 18-year equity boom through the late 1980s and 1990s as boomers swelled the ranks of prime savers.

The worrying bit for the United States is that ratio peaked in 2010.

This may very well be the beginning of the long and painful adjustment suggested in Boom, Bust and Echo. On the academic side, I expect these types of weakening returns to slow retirements, especially as Universities shift more and more to defined contribution pension plans., Mark's excellent post on this makes it rather obvious how unimportant returns are to wealth when they are as low as they are now.

The question is how do we break out of this cycle?

Alternatively, what is the best strategy for those of us who have to try and make some sort of plan for the future under these conditions?

And, finally, with bond yields low and the cost of Social Security baked into the financial system, why is this a good time to talk about privatizing the system? Wouldn't we want to do this in an environment with high rates of return on assets to make the new program have a chance to succeed?

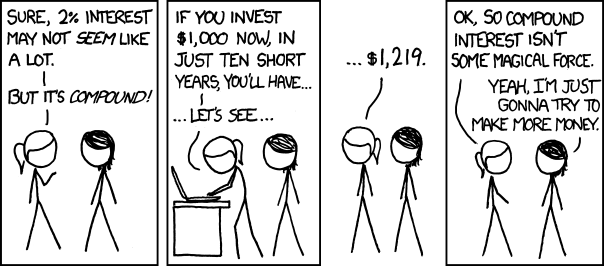

Monday, September 5, 2011

XKCD on investing

What's sad is how frequently a guy with a calculator and basic math skills can take down large chunks of conventional wisdom.

Sunday, September 4, 2011

Cassandra in reverse?

Think about it (no time for full links); by reading that section you could have learned, either from the editorial page proper or from the paper’s favorite op-ed guys, that

Clinton’s tax hike would cause a recession and send stocks plunging

Dow 36,000!

American households are saving plenty thanks to capital gains on their houses

Interest rates will soar thanks to Obama’s deficits

And much, much more.

What’s remarkable is that the Journal does not seem to pay a price for this record of awesome wrongness. Maybe subscribers buy the paper for the reporting (although if you ask me, that’s been going downhill since the Murdoch takeover). But as far as I can tell, lots of people still take the editorial page’s pronouncements seriously, even though it seems likely that you could have made a lot of money by betting against whatever that page predicts.

That really does point to an oddity in human culture. Being wrong does not seem to impact on the authority of the source, at least in some groups. That is an unfortunate property as incorrect predictions should make us rethink our internal models rather than reinforce them.

There are complexities here (everyone will have at least some sort of hit rate as even bad predictions are right every once in a while). But it does seem odd that we often double down on bad ideas.

Friday, September 2, 2011

Because it isn't there

I seem to vaguely recall a time when Americans dreamed up big, ambitious projects.

From NPR's The World:

Dubbeling also insists that the Dutch need a new big engineering project.

“Since we stopped reclaiming land from the sea, we Dutch are in some kind of identity crisis. And in the last decades we could export our ideas. But now, with this economic crisis, we really have to think of something different. ”

A mountain, Dubbeling says, definitely qualifies on that score.

Thursday, September 1, 2011

Credentialing versus teaching

Learning is cheaper and easier than ever. And yet getting a degree is more expensive. How’s that? Something’s off, in a big way. Now of course you can push this too far: “Does Yglesias think we don’t need colleges because people can just look things up on Wikipedia instead?” No, I don’t. But I do remember hearing a lot of bluster from old-line media outlets once upon a time that proved to be completely wrong.

I think that the argument about ease of information transfer is right on. That is why a lot of the argument about higher education have settled into "credentialing" and "signaling". Neither of these functions is easier in the internet age and, to some extent, they may be harder (due to more noise and less signal). That makes it very valuable for universities to be able to do these functions.

The problem, as I see it, is that both tasks can be separated from objective outcomes. If you take a program to learn something then that is a concrete and testable outcome. If you take a program to get a credential, then it is quite possible to divorces this from skills or learning (see mail order college degrees).

That is the function that it gets easy to dilute and that could be a very big deal at some point.

Student Debt

The schools sometimes push these students into high-cost private loans that they can never hope to repay, even when they are eligible for affordable federal loans. Because the private loans have fewer consumer accommodations like hardship deferments, the borrowers often have little choice but to default.

Worse yet, these loans and the bad credit history follow the debtors for the rest of their lives. Even filing for bankruptcy doesn’t clean the slate.

I think the experiment with undischargeable debt has been tried many times over history and it never really ends well. Financing higher education is always going to be tricky (due to the large sums involved and the fact that students do not have a credit history). It also doesn't help that students lack assets so it can be an economically rational decision to accept an early career bankruptcy to discharge a six figure debt.

But the opposite extreme is looking increasingly like a bad idea.

Wednesday, August 31, 2011

Economics puzzle

We researched the 100 U.S. corporations that shelled out the most last year in CEO compensation. At 25 of these corporate giants, we found, the bill for chief executive compensation actually ran higher than the company's entire federal corporate income tax bill.

Accounting games like "transfer pricing" have sent the corporate share of federal revenues plummeting. In 1945, U.S. corporate income taxes added up to 35 percent of all federal government revenue. This year, corporate income taxes will make up just 9 percent of federal receipts. In 1952, the year Republican President Dwight Eisenhower was elected, the effective income tax rate for corporations was 52.8 percent. Last year it was just 10.5 percent.

Among the nation's top firms, the S&P 500, CEO pay last year averaged $10,762,304, up 27.8 percent over 2009. Average worker pay in 2010? That finished up at $33,121, up just 3.3 percent over the year before.

The last is especially puzzling. When salaries rise faster for a specific category of jobs, it tends to signal that the market is finding a shortage of qualified people. It's also the golden time of opportunity for outsiders to break into the market and drop wages.

Or, option B, it is a feature of rent seeking due to a protected market. Which one strikes out humble reader as more likely?

Tuesday, August 30, 2011

A different point of view on Michael Lewis

My favorite part:

Yet, Germany is a prosperous and pleasant nation to live in; one of the best in the world. Germany manages to have lower unemployment than the US, despite all their unions and socialistic regulations for hiring and firing: laws which Harvard economist ding a lings will insist would be the ruination of the American economy. How did the Germans manage this?

The stuff on Iceland is first rate as well. Definitely worth the read.

Saturday, August 27, 2011

More Freakonomics causality

Since the introduction of the ultrasound in Asia, in the early 1980s, it's often been used to determine the gender of a fetus -- and, if it's female -- have an abortion. In a part of the world with big populations, these sex selection abortions have had a big, unintended consequence.The hypothesis that increasing the ratio of men to women would produce "more sex-trafficking, more AIDS, and a higher crime rate" is entirely reasonable, but like so much observational data there's a big self-selection factor here. Families and women not involved in the sex trade tend to avoid rough neighborhoods and red light districts. There's also a question about outliers -- a few very bad areas with very high male to female ratios.Hvistendahl: I mean there are over 160 million females missing from the population in Asia, and to put that in perspective, it's more than the entire female population of the United States.

So, what happens in a world with too many men? For starters, there's more sex-trafficking, more AIDS, and a higher crime rate. In fact, if you want to know the crime rate in a given part of India, one surefire indicator is the gender ratio. The more men, the more crime. Now, the ultrasound machine didn't create these problems, but it did enable them. So, you have to wonder. What's next?

Once again, the suggestion that changing gender ratios would have significant social consequences makes perfect sense, but if you want to go from sensible suggestion to well-supported hypothesis, it's not enough to mention a fact that points in the right direction; you also have to show how other explanations (self-selection, sampling bias, etc.) can't explain away your fact. That, unfortunately, is where Freakonomics and many other economists-explain-the-world books and articles fail to make the grade.