Thank you. I remember, back when I was working for the Treasury, after one White House meeting Joseph Stiglitz—then one of the members of the President's Council of Economic Advisors—turned to me and said:Brad, not every question is best answered with a 10 minute economic history lecture.

But most are.

So let us start in the 1860s with the industrialization of America and the rise of the large scale business enterprise. There is then a law of bankruptcy: when a company does not pay you, and when you cannot work out terms, you go to a judge. The judge bangs his gave. The sheriff then auctions off the company's assets on the sidewalk and the company shuts down.

By the 1890s the judges in New York are saying: "Wait a minute! This makes no sense. Even though it is bankrupt, the New York Central Railroad is much more valuable as a going concern than if we simply pulled the individual rail segments off the roadbed and sold them off as ornamental ironwork. Moreover, there are lots of other stakeholders who rely on the operations of the New York Central--and even though they are not parties, there is a public interest in not having them suffer economic harm." So the judges change the law: they decide that when a large business enterprise goes bankrupt, we the judges will freeze its finances but let its operations continue while people negotiate and design and we approve a plan to restructure its debt and equity so that it can continue to operate. After judges took the lead legislators followed, and so we developed our current law of bankruptcy: when a company declares bankruptcy; we minimize the economic disruption by freezing and then sorting out its finances but letting its operations continue.

This system works pretty well in dealing with the bankruptcies of operating companies. Finances are frozen, debtor-in-possession financing is arranged, operations continue, the lawyers maneuver, and eventually a new financial superstructure is negotiated and plopped down on top of the operating company.

The problem is financial companies. They have no operations. They are all finance. When you freeze the finances the thing dies instantly.

Come the 1930s we face the waves of bank bankruptcies which make the Depression Great. The unemployment rate spikes to a peak non-farm level of 28%. We get the New Deal. The New Deal establishes the FDIC—which exists, among other things, to handle bank failures. When a bank fails the FDIC will go in, pay off its insured deposits, take over its assets and other liabilities, hopefully find a solvent and sound bank to take over the good-bank parts, and eat the remaining losses. This serves as an financial-sector analogue of Chapter 11. The hope was that with the FDIC we will never get into another situation like 1931 in which applying bankruptcy law to failing financial institutions produces general economic disaster.

Tuesday, May 3, 2011

Professor DeLong's history lesson for the day

Apparently, the lot of some economists is to be painfully condescending

The most curious thing about Mr Krugman's quasi-religious squeamishness about the "commercial transaction" is that it is normally the economist's lot to explain to the superstitious public the humanitarian benefits of bringing human life ever more within the cash nexus.Wilkinson's entire post is (unintentionally) interesting and you should definitely take a look at it (though you should also take a look at the rebuttals here and here), but for a distillation of the freshwater mindset, you really can't beat the line about 'the economist's lot.' (I suspect Wilkinson may have been going for humorous wording here but I doubt very much he was joking.)

For a less pithy though perhaps more instructive example, consider these comments Steve Levitt made on Marketplace:

One of the easiest ways to differentiate an economist from almost anyone else in society is to test them with repugnant ideas. Because economists, either by birth or by training, have their mind open, or skewed in just such a way that instead of thinking about whether something is right or wrong, they think about it in terms of whether it's efficient, whether it makes sense. And many of the things that are most repugnant are the things which are indeed quite efficient, but for other reasons -- subtle reasons, sometimes, reasons that are hard for people to understand -- are completely and utterly unacceptable.As I said at the time:

There are few thoughts more comforting than the idea that the people who disagree with you are overly emotional and are not thinking things through. We've all told ourselves something along these lines from time to time.

But can economists really make special claim to "whether [ideas] makes sense"? Particularly a Chicago School economist who has shown a strong inclination toward the kind of idealized models that have great aesthetic appeal but mixed track records? (This is the same intellectual movement that gave us rational addiction.)

When I disagree with Dr. Levitt, it's for one of the following reasons:

I question his analyses;

I question his assumptions;

I question the validity of his models.

Steve Levitt is a smart guy who has interesting ideas, but a number of intelligent, clear-headed individuals often disagree with him. Some of them are even economists.

Monday, May 2, 2011

Another quick one on broadcast TV

Living in Oregon, we have a lot of rainy days, and without the television for the kids to watch on occasion, it could get ugly. I must admit, I am also a primetime junkie, and that is my relaxation time, as well as the time when we all get to sit down and enjoy family time together. So despite how much this service costs, it is one that will always be a part of our budget.As I've mentioned before (a few times), not only is it still possible to watch TV for free, the technology has improved tremendously. The signal is digital and stations can carry multiple channels. I get over a hundred here in LA. In other words, my rabbit ears give me something about one or two steps up from basic cable.

For free.

Of course, a smaller urban center like, say, Portland, Oregon, will have fewer channels but as you can see here, the selection is still pretty good, particularly when compared to the thread-bare line-up from "Comcast Portland Regional - Standard" which not only offers fewer total channels, but also includes just two satellite stations, Discovery and WGN.

Unless you're a Cubs fan or you really like cable access, you'll probably get better programs through an antenna (for example, right now Portland broadcast TV is showing a Sundance winner that's not available on basic cable). You'll also have less image compression, you won't have to deal with the cable company and, just in case this point isn't plain enough, it's FREE!

I'm sure the author wasn't trying to give bad advice here. I'm certain she just didn't know about the other options, but of course that's the problem.

Between cable TV and the internet, consumers are feed an unprecedented stream of advice, but most of it is really bad, an ugly mix of lazy writing, inadequate-to-non-existent research and, worst of all, dependence on the very companies that provide the products and services being purchased.

One consequence of this is that consumers hear almost nothing about options that don't have the backing of a major industry. Another is that narratives are shaped to suit business interests. Check out almost any CNBC clip from say 2007 for excruciating examples.

Sunday, May 1, 2011

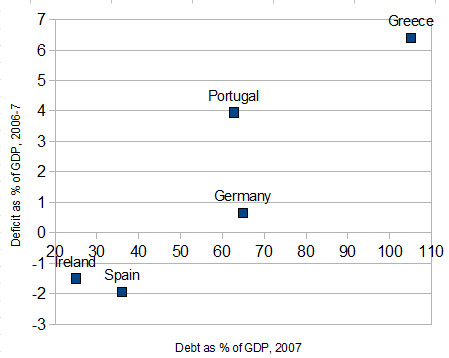

One of Krugman's talents

For example, take the profligate PIGS story -- the EU is in trouble mainly because four countries (Portugal, Ireland, Greece and Spain) were reckless spendthrifts. It's a widespread explanation. Edward Glaeser even used a Spain specific variant of it to argue against high-speed rail.

In response to this, Krugman shows us the debt levels and deficits of these four countries (plus Germany as a reference point) on the eve of crisis:

As Krugman summarizes:

Yes, Greece had big debts and deficit. Portugal had a significant deficit, but debt no higher than Germany. And Ireland and Spain, which were actually in surplus just before the crisis, appeared to be paragons of fiscal responsibility — the former, said George Osborne, was

a shining example of the art of the possible in long-term economic policymaking.

We know now that the apparent fiscal health of Ireland and Spain rested largely on housing bubbles — but that was by no means the official view at the time. And nothing I’ve seen explains how new fiscal rules would prevent a similar crisis from happening again.

Friday, April 29, 2011

Weekend Gaming -- perfecting the imperfect

When the subject of perfect information games comes up, you probably think of chess, checkers, go, possibly Othello/Reversi and, if you're really into board games, something obscure like Agon. When you think of games of imperfect information, the first things that come to mind are probably probably card games like poker or a board game with dice-determined moves like backgammon and, if you're of a nostalgic bent, dominoes.

We can always make a perfect game imperfect by adding a random element or some other form of hidden information. In the chess variant Kriegspiel, you don't know where your opponent's pieces are until you bump into them. The game was originally played with three boards and a referee but the advent of personal computing has greatly simplified the process.

For a less elaborate version of imperfect chess, try adding a die-roll condition to certain moves. For example, if you attempt to capture and roll a four or better, the capture is allowed, if you roll a two or a three, you return the pieces to were they were before the capture (in essence losing a turn) and if you roll a one, you lose the attacking piece. Even a fairly simple variant such as this can raise interesting strategic questions.

But what about going the other way? Can we modify the rules of familiar games of chance so that they become games of perfect information? As far as I can tell the answer is yes, usually by making them games of resource allocation.

I first tried playing around with perfecting games because I'd started playing dominoes with a bluesman friend of mine (which is a bit like playing cards with a man named Doc). In an attempt to level the odds, I suggested playing the game with all the dominoes face up. We would take turns picking the dominoes we wanted until all were selected then would play the game using the regular rules. (We didn't bother with scoring -- whoever went out first won -- but if you want a more traditional system of scoring, you'd probably want to base it on the number of dominoes left in the loser's hand)

I learned two things from this experiment: first, a bluesman can beat you at dominoes no matter how you jigger the rules; and second, dominoes with perfect information plays a great deal like the standard version.

Sadly dominoes is not played as widely as it once was but you can try something similar with dice games like backgammon. Here's one version.

Print the following repeatedly on a sheet of paper:

Each player gets as many sheets as needed. When it's your turn you choose a number, cross it out of the inverted pyramid then move your piece that many spaces. Once you've crossed out a number you can't use it again until you've crossed out all of the other numbers in the pyramid. Obviously this means you'll want to avoid situations like having a large number of pieces two or three spaces from home.

Each player gets as many sheets as needed. When it's your turn you choose a number, cross it out of the inverted pyramid then move your piece that many spaces. Once you've crossed out a number you can't use it again until you've crossed out all of the other numbers in the pyramid. Obviously this means you'll want to avoid situations like having a large number of pieces two or three spaces from home.If and when you cross off all of the numbers in one pyramid you start on the next. There's no limit to the number of pyramids you can go through. Other than that the rules are basically the same as those of regular backgammon except for a couple of modifications:

You can't land on the penultimate triangle (you'd need a one to get home and there are no ones in this variant);

If all your possible moves are blocked, you get to cross off two numbers instead of one (this discourages overly defensive play).

I haven't had a chance to field test this one, but it should be playable and serve as at least a starting point (let me know if you come up with something better). The same inverted pyramid sheet should be suitable for other dice based board games like parcheesi and maybe even Monopoly (though I'd have to give that one some thought).

I had meant to close with a perfected variant of poker but working out the rules is taking a bit longer than I expected. Maybe next week.

In the meantime, any ideas, improvement, additions?

A physicist in econ-land

Noah Smith has some fascinating things to about making the transition to economics as a grad student (via Thoma, of course):

At the time I took the course, I didn't yet know enough to have any of these objections. But coming as I did from a physics background, I found several things that annoyed me about the course (besides the fact that I got a B). One was that, in spite of all the mathematical precision of these theories, very few of them offered any way to calculate any economic quantity. In physics, theories are tools for turning quantitative observations into quantitative predictions. In macroeconomics, there was plenty of math, but it seemed to be used primarily as a descriptive tool for explicating ideas about how the world might work. At the end of the course, I realized that if someone asked me to tell them what unemployment would be next month, I would have no idea how to answer them.

As Richard Feynman once said about a theory he didn't like: "I don’t like that they’re not calculating anything. I don’t like that they don’t check their ideas. I don’t like that for anything that disagrees with an experiment, they cook up an explanation - a fix-up to say, 'Well, it might be true.'"

That was the second problem I had with the course: it didn't discuss how we knew if these theories were right or wrong. We did learn Bob Hall's test of the PIH. That was good. But when it came to all the other theories, empirics were only briefly mentioned, if at all, and never explained in detail. When we learned RBC, we were told that the measure of its success in explaining the data was - get this - that if you tweaked the parameters just right, you could get the theory to produce economic fluctuations of about the same size as the ones we see in real life. When I heard this, I thought "You have got to be kidding me!" Actually, what I thought was a bit more...um...colorful.

Update: Krugman chimes in with some relevant comments here.

"Premature Ecalculation"

As is usually the case with journalistic hypocrisy, the best rebuttal comes from the Daily Show.

Thursday, April 28, 2011

Inessential Yglesias -- understanding the elasticity of oil demand

For example:

However there are important caveats to these estimates that suggest the real current elasticity is higher. First, the evidence has indicated that the response of demand to price changes is asymmetric: price increases cause a larger response to demand than price decreases. This is because price increases are more likely to cause shifts to newer, more energy efficient technologies than price decreases are to undo such shifts. Any estimate of the average price elasicity then will be a downward biased estimate for the likely response to a price increase.

A recent paper by Davis and Killian The Journal of Applied Economics covers some other econometric issues in the literature. For instance, we know price and quantity demanded are jointly determined, which means that there will be a correlation between the price variable and the errors such that single equation or panel data methods, like those used in the reported IMF estimates, will bias estimates towards zero. Some studies attempt to use exogeneous oil shocks as instrumental variables. This approach is used in the appendix to the IMF study. But this requires the assumption that consumers will respond the same to these shocks as to normal real price appreciation. If consumers expect shocks to be more temporary than a demand led increase in price, this is a questionable assumption.

To understand why this is such an important point, we need to step back and discuss why we choose certain analytic approaches in certain situations, specifically why we shouldn't think about elasticity of demand for gasoline the same way we think about it for fruit juice.

[brief warning: I'm a statistician, not an economist, so the terminology here might not be what you'd hear in INTRO TO ECON, but I suspect the underlying concepts will be basically the same.]

Let's discuss demand in terms of decisions. If I go into the grocery store thinking I'd like some orange juice I almost certainly have some threshold price X in mind. If a carton of juice costs more than X, I won't buy orange juice that day.

Assuming I don't have some sort of weird Minute Maid fixation, doing without juice is probably not a big deal. My consumption is determined by a single simple (rather than complex) decision.

[brief warning II: I'm assuming, for the sake of simplicity, that all the grocery stores and gas stations available to me charge roughly the same prices for comparable items.]

By comparison, my consumption of gasoline is determined by a complex set of decisions spread out over a long time and based on anticipated gas prices. Of these decisions, the impact of the one that's analogous to the OJ decision (go to the store and check the price) is trivial next to choosing where do I live, where do I work and what kind of vehicle do I drive.

Even if there is a there happens to be a hurricane or a revolution at the exact time I'm making one of those decisions and gas is at five dollars a gallon, I probably won't bother factoring that in. Trying to estimate the impact of temporary and unpredictable events is a game best left to the specialists.

But let's say that the five dollar price is the result of a recent buck and a half increase in the gas tax and I only see it going north from here. Now five dollars a gallon is starting to look like a floor instead of a ceiling and I am much more more likely to look at MPG and commuting distance when I make my decisions.

Or, in other words, pretty much what Ozimek said.

Essential Yglesias

One is that while low elasticity implies that a tax is unlikely to be very effective at reducing demand, by the exact same token a low elasticity implies that taxing whatever it is you’re proposing to tax will be a very efficient way of raising revenue. So if you’re the kind of person who believes the government should raise revenue, then there’s really no possible result in the elasticity literature that should make you hesitate to tax gasoline and/or oil.

The other thing is that these elasticity estimates generally imply that the relationship between price and demand is going to be linear, which is almost certainly false. Which is to say that the estimate is only reliable when you’re considering a relatively small policy shift. Nothing wrong with that, there’s just no way to get an empirical estimate about some crazy shift outside the realm of ordinary experience. But it is a real limitation to what this kind of work can tell us.

The second point, that relationships like these are unlikely to be linear is a theme that Mark has been trying to communicate for years and it is nice to see the idea beginning to get traction.

But the first point is a really good one. I like government (not unlimited government, but unlimited ice cream is bad for me too) and I recognize that we need to raise revenue somehow. If the tax on fuel consumption is a way to raise revenue that is a major benefit.

Now it is true that this could adversely impact the transportation options of the less well off. But there are a number of options including means tested fuel tax credits and improved public transportation infrastructure that could be tried. But I think the bottom line is that this tax is like alcohol and cigarette taxes -- we want to discourage an activity and raise revenue for basic services at the same time; while it isn't optimal tax policy (which might address issues like the capital gains tax) it is a major improvement.

Wednesday, April 27, 2011

Around a quarter of a million reasons to want to keep your job

I had always thought of this as a Southern problem, but this excellent piece by Dana Goldstein has me questioning that assumption:

One of Governor Andrew Cuomo's contentious budget cutting ideas is to consolidate very small school districts. I'm generally a tax-and-spend liberal, but this is a good idea, especially in relatively densely-populated parts of the state. I was reminded why today by the New York Times, which reported on a controversy engulfing the tiny Westchester village of Katonah, NY, not far from where I grew up. Katonah's school board would like to hire a superintendent named Paul Kreutzer, who happens to be the only superintendent in Wisconsin to have publicly supported Gov. Scott Walker's attempt to ban teacher collective bargaining.

Unsurprisingly, hundreds of Katonah teachers, parents, and students are loudly protesting Kreutzer's appointment.

But what really caught my eye was that if he does get the job, the 39-year old Kreutzer is set to earn $245,000 annually to oversee a district of just six schools and 3,800 students. Ninety-three percent of these kids are white, and just 1 percent are non-native English speakers. Approximately 0 percent of Katonah public school children participate in the federal free-and-reduced-price lunch program.

This reminds me of an anecdote I've mentioned here before.

When I first decided to go into teaching I asked a retired superintendent I knew for advice. The first thing he told me was, "Never trust a superintendent; they'll lie to your face." I think he was being just a bit harsh but I understand his position. Administrators live in an intensely political world where the right move can double their incomes and the wrong one can get them demoted or fired. It tends to test character.

Just to be clear, like teachers, most administrators (particularly most principals) are dedicated educators who genuinely care about their students, but they are also, by necessity, expert game-players who know how to work a system. This is simply part of the skill set. An administrator who's bad at politics will probably be a bad administrator.

But if we can't blame administrators for being good at politics, we can certainly blame many education reporters for being bad at journalism. To the extent that this is a story of labor and management, most journalists have unquestioningly swallowed the line of certain managers* that the blame for any problems in the system rested entirely with labor. Every standard of good journalism should have told them to look at both sides of the issue. Every reporter's instinct should have told them to take with a block of salt potentially self-serving claims of a group of media savvy, politically adept people who are trying to protect high but vulnerable salaries and, in some cases, impressive potential careers in politics and the private sector.

* And to be ABSOLUTELY clear, let me make this point explicitly: I am not talking about most administrators. The majority of superintendents and the vast majority of principals are hard-working and intensely focused professionals whose first priority is the interests of their kids. Just like the vast majority of teachers.

Preblog -- Businessmen seldom believe in efficient markets and rational actors

Back in my marketing days when I was building consumer response models and working with the BAs, we would talk about maximizing the perceived to real value ratio -- find a cheap product that looked expensive. Like many, if not most, of our strategies and business plans, this idea was based on assumptions that violated some of the axioms of freshwater economics.

Efficiency and rationality are useful for businesses for lobbying and PR purposes but most people in the private sector don't believe in them. They think can beat the system. That's why they're there.

* nicely rebutted here and here.

Tuesday, April 26, 2011

Two quotes

On top of that, Wall Street does have a habit of boiling everything down to a right/wrong duality: if you say that a stock will go down, you’re right if it does, and wrong if it doesn’t. The intelligence of your analysis, or the idea that all these things are probabilistic rather than certain, rarely even gets lip service. This is why you see so much technical analysis on Wall Street: it makes no intellectual sense at all, but it works just as well as — or even better than — fundamentals-based analysis. (Which, admittedly, isn’t saying very much.) And that’s all that matters.Felix Salmon

All in all I’d rather have been a judge than a miner. And what is more, being a miner, as soon as you are too old and tired and sick and stupid to do the job properly, you have to go. Well, the very opposite applies with the judges.Peter Cook via Krugman

Subtracted cities -- the art of falling gracefully

I once mentioned this to a colleague who had drank deeply of the Kool-aid. I expected one of two responses: either he would find this troubling or he would point out a flaw in my argument. He did neither. Instead he just shrugged and smiled and assured me that when we reached that point the people who ran the company would simply find a way to "innovate out of the problem."

It's easy to understand the appeal of growth but good planning and management also have to be able to handle plateaus and even declines. This is true for industries like the newspaper business. It's also true for cities.

From Deborah Potter via Richard Green by way of Mark Thoma:

Detroit stands as the ultimate expression of industrial depopulation. The Motor City offers traffic-free streets, burned-out skyscrapers, open-prairie neighborhoods, nesting pheasants, an ornate-trashed former railroad station, vast closed factories, and signs urging "Fists, Not Guns." A third of its 139 square miles lie vacant. In the 2010 census it lost a national-record-setting quarter of the people it had at the millennium: a huge dip not just to its people, but to anxious potential private- and public-sector investors.

Is Detroit an epic outlier, a spectacular aberration or is it a fractured finger pointing at a horrific future for other large shrinking cities? Cleveland lost 17 percent of its population in the census, Birmingham 13 percent, Buffalo 11 percent, and the special case of post-Katrina New Orleans 29 percent. The losses in such places and smaller ones like Braddock, Penn.; Cairo, Ill.; or Flint, Mich., go well beyond population. In every recent decade, houses, businesses, jobs, schools, entire neighborhoods -- and hope -- keep getting removed.

The subtractions have occurred without plan, intention or control of any sort and so pose daunting challenges. In contrast, population growth or stability is much more manageable and politically palatable. Subtraction is haphazard, volatile, unexpected, risky. No American city plan, zoning law or environmental regulation anticipates it. In principle, a city can buy a deserted house, store or factory and return it to use. Yet which use? If the city cannot find or decide on one, how long should the property stay idle before the city razes it? How prevalent must abandonment become before it demands systematic neighborhood or citywide solutions instead of lot-by-lot ones?

Subtracted cities can rely on no standard approaches. Such places have struggled for at least two generations, since the peak of the postwar consumer boom. Thousands of neighborhoods in hundreds of cities have lost their grip on the American dream. As a nation, we have little idea how to respond. The frustratingly slow national economic recovery only makes conditions worse by suggesting that they may become permanent.

Subtracted cities rarely begin even fitful action until perhaps half the population has left. Thus generations can pass between first big loss and substantial action. Usually the local leadership must change before the city's hopes for growth subside to allow the new leadership to work with or around loss instead of directly against it. By then, the tax base, public services, budget troubles, labor forces, morale and spirit have predictably become dismal. To reverse the momentum of the long-established downward spiral requires extraordinary effort. Fatalism is no option: Subtracted cities must try to reclaim control of their destinies. ...

While we're on the subject of economic assumptions...

I was catching up on some old Planet Money episodes and caught Allen Sanderson of the University of Chicago talking about how to allocate scarce resources. The first day of introductory economics, he says, there are always more students than seats. Say there are forty extra people, and he can only accept ten more into the class. He asks the class: how should the ten slots be allocated? You can easily guess the typical suggestions: by seniority, because seniors won’t be able to take the class later; by merit (e.g., GPA), because better students will contribute more to the class and get more out of it; to the first ten people outside his office at 8 am the next day, since that is a proxy for desire to get in; randomly, since that’s fair; and so on. Someone also invariably suggests auctioning off the slots.This, Sanderson says, illustrates the core tradeoff of economics: fairness and efficiency. If you auction off the slots, they will go to the people to whom they are worth the most, which is best for the economy as a whole.* If we assume that taking the class will increase your lifetime productivity and therefore your lifetime earnings by some amount, then you should be willing to pay up to the present value of that increase in order to get into the class. An auction therefore ensures that the slots will go to the people whose productivity will go up the most. But of course, this isn’t necessarily fair, especially when you consider that the people who will get the most out of a marginal chunk of education are often the people who have the most already.

...

But I think the picture is still a bit more complicated. Even if we assume for a moment that allocative efficiency is the only thing we care about, it’s far from clear than an auction will give it to us. If people could (a) predict their increased productivity from taking the class, (b) predict their increased lifetime earnings, (c) discount those earnings to the present (which implies knowing the proper discount rate), and (d) borrow up to that amount of money at the risk-free rate, then, yes, everything would work out OK. But this is clearly not the case, since then people would be bidding thousands if not tens of thousands of dollars to get into the class.

Still, you might say that people’s willingness to pay for the class — even if it’s just that one person is willing to pay $60 and another is only willing to pay $5 — is a valid proxy for the value of the class to them. So instead of thinking in terms of lifetime productivity, we’re thinking of the class as a short-term consumption good, and it would provide $60 of utility to one person and $5 of utility to the other. (Note that we’ve given up the idea of maximizing the ultimately economic impact of the class.) But then we have to ask whether money is a valid proxy for utility, and at this point the chain of reasoning breaks down. My willingness to pay for various goods might reflect their relative utility to me, but saying that different people’s willingness to pay for the same good reflects the relative utility of that good to those people is a much greater leap. Most obviously, a rich person will be willing to pay more for some goods than a poor person, even if those goods would provide more utility to the poor person. Assume for example that the rich person has a wool overcoat, the poor person has no overcoat, and the good in question is a cashmere overcoat.